-

×

1 Hour SEO | Become a Technical Marketer

1 × $40.00

1 Hour SEO | Become a Technical Marketer

1 × $40.00 -

×

Trial Guides - Roundtable Q&A with David Ball, Artemis Malekpour, and Keith Mitnik

1 × $15.00

Trial Guides - Roundtable Q&A with David Ball, Artemis Malekpour, and Keith Mitnik

1 × $15.00 -

×

Teach Yourself - Vietnamese

1 × $17.00

-

×

16 Seminar Home Study Course – Lawrence G. McMillan

1 × $60.00

-

×

Certified Clinical Anxiety Treatment Professional (CCATP) Training Course: Applied Neuroscience for Treating Anxiety, Panic, and Worry - Catherine M. Pittman

1 × $125.00

-

×

$200k Book Blueprint Training – Richelle Shaw

1 × $96.00

Trial Guides - Roundtable Q&A with David Ball, Artemis Malekpour, and Keith Mitnik

Trial Guides - Roundtable Q&A with David Ball, Artemis Malekpour, and Keith Mitnik  $200k Book Blueprint Training – Richelle Shaw

$200k Book Blueprint Training – Richelle Shaw

Original price was: $367.00.$69.00Current price is: $69.00.

You will create different mean reversion strategies such as Index Arbitrage, Long-short portfolio using market data and advanced statistical concepts. A must-do course for quant traders.

Purchase this course you will earn

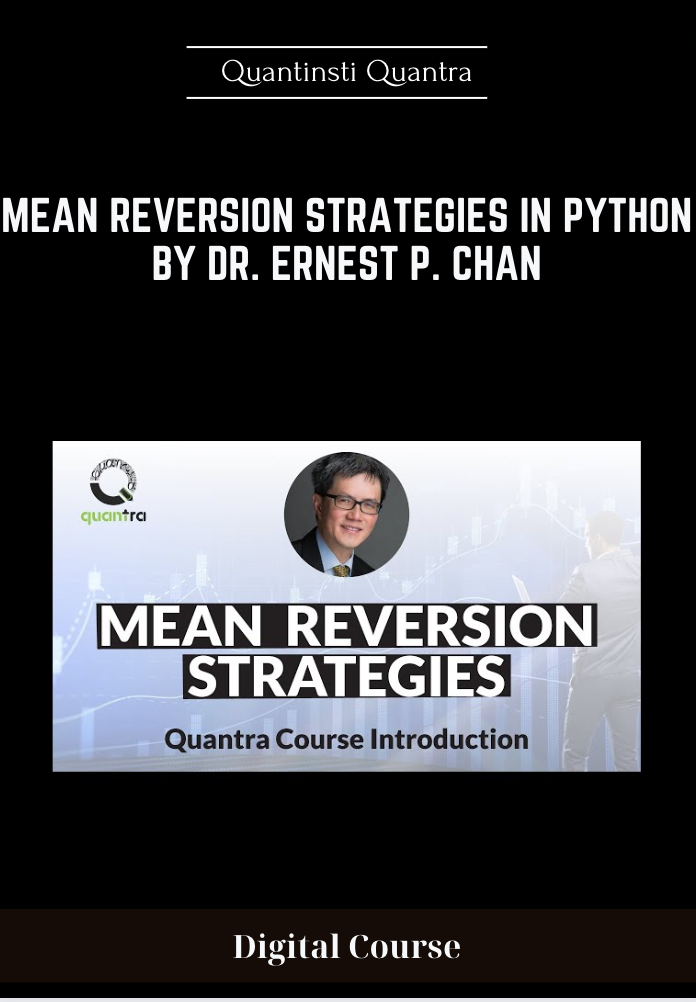

Purchase this course you will earn Elevate your skills with the Mean Reversion Strategies In Python by Dr. Ernest P. Chan – Quantinsti Quantra course, available for just Original price was: $367.00.$69.00Current price is: $69.00. on Utralist.com! Browse our curated selection of over 60,000 downloadable digital courses across diverse Forex and Trading. Benefit from expert-led, self-paced instruction and save over 80%. Start learning smarter today!

Salepage link: At HERE. Archive: https://archive.is/B3O96

Total sizes: 216 MB – include:

Buy now $69 $367, Mean Reversion Strategies In Python by Dr. Ernest P. Chan – Quantinsti Quantra Course.

Mean Reversion Strategies In Python

Offered by Dr. Ernest P Chan, this course will teach you to identify trading opportunities based on Mean Reversion theory. You will create different mean reversion strategies such as Index Arbitrage, Long-short portfolio using market data and advanced statistical concepts. A must-do course for quant traders.

APPLY MEAN REVERSION STRATEGIES

Create four different types of mean reverting strategies

Perform statistical test for identifying stationarity and co-integration

Backtest pairs trading, triplets, index arbitrage and long-short strategy

Explain the role of risk management

Paper trade and live trade your strategies without any installations or downloads

MEAN REVERSION TRADING COURSE

Introduction to the Course

This section gives an overview of the mean reversion strategy through examples. You will go through the course structure and understand how the course is structured in videos, quizzes, strategy codes and interactive coding exercises. This will make sure that not only do you understand the mechanics of mean reversion but also implement trading strategies in live markets.

Introduction by Dr. Ernest Chan

Introduction to Mean Reversion Strategy

Course Structure Flow Diagram

Quantra Features and Guidance

Types of Statistical Arbitrage Strategies

Stationarity of Time Series

Augmented Dickey-Fuller Test

Mean Reversion Strategy

Live Trading on Blueshift

Live Trading Template

Cointegration

Pairs Trading

Triplets

Half Life

Risk Management

Best Markets to Pair Trade

Index Arbitrage

Long Short Portfolio

Run Codes Locally on Your Machine

Automated Trading Using IBridgePy

Summary

ABOUT AUTHOR

Dr. Ernest P. Chan

Dr. Ernest Chan is the Managing Member of QTS Capital Management, LLC., a commodity pool operator and trading advisor. QTS manages a hedge fund as well as individual accounts. He has worked in IBM human language technologies group where he developed natural language processing system which was ranked 7th globally in the defense advanced research project competition. He also worked with Morgan Stanley’s Artificial intelligence and data mining group where he developed trading strategies.

Cultivate continuous growth with the Mean Reversion Strategies In Python by Dr. Ernest P. Chan – Quantinsti Quantra course at Utralist.com! Unlock lifetime access to premium digital content, meticulously designed for both career advancement and personal enrichment.

- Lifetime Access: Enjoy limitless access to your purchased courses.

- Exceptional Value: Benefit from savings up to 80% on high-quality courses.

- Secure Transactions: Your payments are always safe and protected.

- Practical Application: Gain real-world skills applicable to your goals.

- Instant Accessibility: Begin your learning journey immediately after buying.

- Device Compatible: Access your courses seamlessly on any device.

Transform your potential with Utralist.com!

| Status | |

|---|---|

| Total size | |

| Language | |

| Author |

Related products

Forex and Trading

Original price was: $110.00.$43.00Current price is: $43.00.

Forex and Trading

Original price was: $1,995.00.$91.00Current price is: $91.00.

Forex and Trading

Original price was: $175.00.$35.00Current price is: $35.00.

Forex and Trading

Elliott Wave The Futures Junctures Technical Toolbox – Jeffrey Kennedy

Original price was: $237.00.$75.00Current price is: $75.00.

Forex and Trading

Ultimate Day Trading Strategy – Raghee Horner – Simpler Trading

Original price was: $597.00.$79.00Current price is: $79.00.

Forex and Trading

Original price was: $1,197.00.$232.00Current price is: $232.00.

Forex and Trading

Original price was: $1,399.00.$312.00Current price is: $312.00.